Companies often outsource the organization of their finances to independent professionals, then hire accountants for more complex issues and tax filing. If not done at the time of the transaction, the bookkeeper will create and send invoices for funds that need to be collected by the company. The bookkeeper enters relevant data such as date, price, quantity and sales tax (if applicable). When this is done in the accounting software, the invoice is created, and a journal entry is made, debiting the cash or accounts receivable account while crediting the sales account. Poor financial management is one of the primary reasons for small difference between insolvency & negative equity business failure, especially in the first year of the business.

Owners of small businesses need to plan how they allocate their limited resources including labor, machinery, equipment, and cash towards accomplishing their business objectives.

As stated previously, the product of bookkeeping is financial statements.

This type of analysis allows you to focus on your company’s strengths and improve on its weaknesses.

The double-entry method begins with a journal, followed by a ledger, a trial balance, and financial statements.

Difference between Bookkeeping and Accounting

A QuickBooks Live Bookkeeper can help ensure that your business’s books close every month, and you’re primed for tax season. Our experts—CPAs and QuickBooks ProAdvisors—average 15 years of experience working with small businesses across industries. You can nonprofit board president responsibilities record transactions by hand in a journal or a Microsoft Excel spreadsheet.

Wave provides a cloud-based solution for businesses looking to do their bookkeeping themselves. It’s a great choice if you’d like to manage your finances from anywhere and won’t require additional assistance. Bookkeeping is important because it documents every transaction that occurs within your company.

Cash-Based Accounting

Along with hiring an accountant, small business owners increasingly use online accounting software like FreshBooks. With FreshBooks’ user-friendly cloud-based mobile interface, you can access integrated double-entry accounting features from any device, even on the go. We make it easy to take control of your business and manage your bookkeeping safely, from anywhere.

Single vs. Double-Entry Bookkeeping: What’s Best for Your Business?

With well-managed bookkeeping, your business can closely monitor its financial capabilities and journey toward heightened profits, breakthrough growth, and deserved success. It’s the meticulous art of recording all financial transactions a business makes. And it gets you on the path to transform your business into a money-maker. Petty cash is a small amount of money that your business uses for different purposes throughout the day. This could be as simple as buying doughnuts for your office or grabbing lunch during an impromptu meeting. To keep track of these expenses, you’ll need to use the petty cash bookkeeping method.

It Helps You Make Better Decisions

Bookkeeping is important because it allows you to take control of your business’ finances. You will benefit from paying your bills on time and receiving payment for your products or services on time too. Its this delicate balance of cash inflow and outflow that will keep your business going. By definition, bookkeeping is the organization of financial information.

There’s good news for business owners who want to simplify doing their books. Business owners who don’t want the burden of data entry can hire an online bookkeeping service. These services are a cost-effective way to tackle the day-to-day bookkeeping so that business owners can focus on what they do best, operating the how is inherent risk assessed by an auditor business. For business owners who don’t mind doing the data entry, accounting software helps to simplify the process. You no longer need to worry about entering the double-entry data into two accounts.

If you find yourself needing to implement a bookkeeping process, consider hiring a bookkeeping professional to help. Last, but certainly not least, the law requires you to keep financial records for your company. Depending on your legal structure, the law requires you to keep financial records separate from your personal expenses. Tactical and strategic planning is the core of what you do as a business owner. With bookkeeping as a tool, you are closer to your short and long-term goals.

As a business owner, it is important to understand your company’s financial health. Bookkeeping puts all the information in so that you can extract the necessary information to make decisions about hiring, marketing and growth. The first method of accounting is the cash-based accounting method. This method records financial transactions when money is exchanged. This means that you don’t record an invoice until it is actually paid.

By understanding and accurately recording unearned revenue, businesses can better manage cash flow and service obligations to their customers. Admiral’s UK motor quota share contracts operate on a funds withheld basis, with Admiral retaining ceded premium (net of the reinsurer margin) which then covers claims and expenses. If an underwriting year is not profitable, investment income is allocated to the withheld fund and used to delay the point at which cash recoveries are collected retained earnings from the reinsurer.

Deferred Revenue Recognition Compliance

Be careful with your unearned revenue, though, as tax authorities across the globe have specific requirements for recognizing unearned revenue, and flouting these rules is a good way to get audited. Securities and Exchange Commission (SEC) that a public company must meet to recognize revenue. No material provisions have been made in these financial statements in relation to the matters noted above. The model has been calibrated on historical data that may not fully reflect the risk of losses in the recent and ongoing, highly volatile macro-economic period.

Revenue Recognition Principle

The application of the amendments listed above has not had a material impact on the Group’s results, financial position and cashflows.

When a company receives payment before rendering the service or delivering the product, it must recognize this receipt as a liability on its balance sheet.

This is important for understanding a company’s overall financial condition.

The correlation of assumptions will have a significant effect in determining the ultimate impacts, but to demonstrate the impact due to changes in each assumption, assumptions have been changed on an individual basis.

Given the Group’s very strong capital position, this is comfortably absorbed.

Supply chain pressures across the global repair network led to slower damage repair times during 2022 and early 2023, resulting in service pressures across the industry.

Current liabilities of a company consist of short-term financial obligations that are typically due within one year. Current liabilities could also be based on a company’s operating cycle, which is the time it takes to buy inventory and convert it to cash from sales. Current liabilities are listed on the balance sheet under the liabilities section and are paid from the revenue generated from the operating activities of a company. Unearned revenue can provide clues into future revenue, although investors should note the balance change could be due to a change in the business.

Unearned revenue in the cash accounting system

Consider a media company that receives a $1,200 advance payment at the beginning of its fiscal year from a customer who’s purchasing an annual newspaper subscription. Upon receipt of the payment, the company’s accountant records a debit entry to the cash and cash equivalent account and a credit entry to the deferred revenue account for $1,200. The other company involved in a prepayment situation would record their advance cash outlay as a prepaid expense or an asset account on their balance sheet. The other company recognizes its prepaid amount as an expense over time at the same rate as the first company recognizes earned revenue.

Unearned revenue plays a crucial role in accrual accounting, as it represents cash received from customers for services or products that have not yet been delivered.

Because a company cannot recognize revenue on this cash advance and because it owes money to a customer, it must record a current liability for any portion of the cash advance for which it expects to provide services within a year.

This decreases your unearned revenue liability because you performed the service.

However, if one company’s debt is mostly short-term debt, it might run into cash flow issues if not enough revenue is generated to meet its obligations.

ConTe also achieved the highest NPS in the industry and the best Trustpilot score for online insurance, largely reflecting our excellent operational service levels.

AccountingTools

This means unearned revenue is listed as a liability on your balance sheet until your business delivers the promised services or goods. Unearned revenue should be entered into your journal as a credit to the unearned revenue account and as a debit to the cash account. This journal entry illustrates that your business has received cash for its service that is earned on credit and considered a prepayment for future goods or services rendered.

Unearned revenue is reported on a business’s balance sheet, an important financial statement usually generated with accounting software. If a business entered unearned revenue as an asset instead of a liability, then its total profit would be overstated in this accounting period. The accounting period were the revenue is actually earned will then be understated in terms of profit. It’s categorized is unearned revenue a current liability as a current liability on a business’s balance sheet, a common financial statement in accounting. Deferred revenue is typically reported as a current liability on a company’s balance sheet because prepayment terms are typically for 12 months or less. Generally accepted accounting principles (GAAP) require certain accounting methods and conventions that encourage accounting conservatism that ensures that the company is reporting the lowest possible profit.

More human research is needed to understand how alcohol affects hunger. One animal study published in 2017 found that alcohol activates cells in your brain that signal intense hunger. While alcohol doesn’t necessarily affect everyone the same way, it can cause some people to gain weight due to its high-calorie content and the way it affects metabolism, hunger-hormones, and decision making.

She is past chair of the ACLM’s registered dietitian member interest group, secretary of the women’s health member interest group, and nutrition faculty for many of ACLM’s other course offerings.

If the drinker compensates for the calories in alcohol by decreasing calorie intake from food, this would explain the lack of weight change with moderate drinking.

In this article, we describe how alcohol can cause a bloated appearance in the stomach.

This is important for potential weight gain because it dictates how your body reacts to alcohol.

Eliminating or reducing alcohol consumption is a common dieting behavior.

Still, the study suggests that cutting out alcohol isn’t a reliable way to lose weight in the short term, and, over the course of years, may only have a small effect at most.

Alcohol Intake and Obesity: Potential Mechanisms

Aside from the immediate influence on appetite that comes from alcohol consumption, there are also effects on energy storage. Alcohol inhibits fat oxidation, suggesting that frequent alcohol consumption could lead to fat sparing, and thus higher body fat in the long term 62. However, the results of the various cross-sectional and longitudinal studies examined in this review do not unequivocally support such a hypothesis. Finally, there is also evidence to suggest that traits that predispose individuals to binge drinking may also predispose to binge eating 66. Prospective studies have looked at the association between alcohol intake and adiposity gain in various populations, with follow-up periods ranging from several months to 20 years 4, 30, 31.

Tips for Mindful Drinking to Support Weight Management

It has also been suggested that some of the energy ingested as alcohol is ‘wasted’, due to the activation of the inefficient hepatic microsomal ethanol-oxidizing system (MEOS). The MEOS is induced through chronic alcohol intake, and the level of induction increases with increased intake 54, 67. Oxidation of alcohol via the MEOS produces less ATP than oxidation via alcohol dehydrogenase, using the energy from alcohol intake primarily to enhance heat production 37, 54. The extent to which wasted energy from regular alcohol consumption contributes to weight gain prevention is unclear.

The connection between alcohol and weight gain is a lot more tenuous than you’d think.

As a result, people who drink heavily may have high cortisol levels.

Cirrhosis, on the other hand, is irreversible and can lead to liver failure and liver cancer, even if you abstain from alcohol.

Eating food while drinking can help slow the absorption of alcohol, but some foods can also increase the risk of bloating, including fatty foods.

Alcohol also reduces inhibition and good decision-making, meaning you are much more likely to throw your healthy eating plan straight out of the window and make nachos after you’ve had a few.

So you’ve had a rough night out, and the only remedy is to stress eat donuts, burgers, and crisps all afternoon while lying on the couch under a blanket of shame. You’re stressed, so you’ll likely crave junk food to feel better again. Let’s say you wake up with terrible anxiety or a mind full of regrets from last night’s behavior. You’ve doubled the recommended caloric intake of an entire day in the span of a few hours. Now that alcohol is in your body, it is being converted to acetate, which your body LOVE, LOVE, LOVES. Or maybe you’ve had a rough day and treated yourself to half a standard bottle of Rosé.

Alcohol and weight gain

You’ve likely considered what you’re eating, what you’re not eating and of course, how much you’re moving. And if you drink alcohol, you may have thought about that as well. Alcohol spikes cortisol levels in the body, which contributes to the accumulation of belly fat. It also impedes your ability to get a good night’s sleep, further contributing to belly fat. That’s an additional 2,000-3,000 calories of fatty, salty, nutritionally poor food sitting in your stomach, which is still reeling from the 4,000+ nighttime calories you crammed into it less than 12 hours ago.

Mindful Eating Strategies for the Holiday Season

Overall, the empty calories that come from alcoholic drinks are a significant contributor to gaining weight from alcohol. In the cohort studies, the researchers found no significant association between people who drank alcohol and weight gain, regardless of how much they drank. You may already be aware of some of the more unsavory side effects of alcohol, especially when you overdo it. It can increase anxiety, heighten your blood pressure and even affect your brain.

Red Wine (105 Calories per 5 oz Serving)

Alcohol consumption can also interfere with your digestive system. It may slow down the digestion process and cause temporary gastrointestinal disturbances such as gas or constipation. These disruptions contribute to a feeling of heaviness and can make your weight measurement a bit higher than usual.

Hormone therapy usually is used to help with hot flashes that affect quality of life.

A 2023 study found that alcohol consumption contributes to fat deposits around the body, including the stomach, which can cause a bloated appearance.

While your body deals with metabolizing and eliminating the toxic alcohol, all of the food you just ate (or ate semi-recently) will likely end up being stored as fat. Alcohol contains 7 calories per gram, which is more than carbohydrates and protein (4 kcal/g) but less than fat (9 kcal/g). “Across the board, for people who are trying to lose some weight, cutting out empty calories is a good place to start,” emphasizes Dr. Heinberg. Pancreatitis can be a short-term (acute) condition that clears up in a few days. But prolonged alcohol abuse can lead to chronic (long-term) pancreatitis, which can be severe.

How to get rid of alcohol bloating

Research has found that elevated cortisol levels may increase abdominal weight gain. Cortisol redistributes fat tissue to your abdominal region and increases cravings for high-calorie foods. Weight is certainly not the only factor when it comes to health. Still, there are a few things you may want to know does rum make you gain weight about alcohol intake and body composition if you think drinking may affect your weight.

The financial reporting segment takes the same data from revenue management and compiles reports instantly for quick review. Under the financial management segment, you can make intercompany entries and manage workflows and content management. It allows adjustments to be made easily and can provide month-end and year-end reporting quickly.

Automate Invoicing and Expense Tracking

Essentially, this ASU improves disclosure requirements, prompting more useful information out of financial statements. The FASB put it in place to ensure companies provide more transparency into how they recognize their revenues. Now that you know how company accounting is different, let’s get into the nitty-gritty of accounting for contractors. To record a construction cost, debit the construction in the process column and The Role of Construction Bookkeeping in Improving Business Efficiency credit the cash column.

In contrast, construction companies face a different and much more complicated series of challenges.

We turned to popular sites, including Trustpilot, G2 and Capterra, for these customer responses.

The reporting will enable you to track the profitability of each project so that you can stay ahead of costly mistakes.

So far in this construction company accounting guide, we have covered payrolls, billing, and revenue recognition.

When it comes to real estate management, the platform takes static information, such as lease contracts, and transforms them into dynamic information resources.

Reasons to Hire a Bookkeeper for Your Small Business

Implement robust cash flow forecasting and management practices to ensure your business remains financially healthy. Regular account reconciliation helps catch errors, prevent fraud, and ensure accurate financial reporting. Despite these differences, construction accounting still adheres to general accounting principles and requires accurate record-keeping, financial statements, and tax compliance.

Streamline Your Finances: Download Our Free Bookkeeping Brochure

Effective construction bookkeeping is not just a compliance necessity; it’s a strategic asset that drives profitability, fuels growth, and empowers informed decision-making. Working with a certified bookkeeper or accountant specializing in construction accounting can greatly benefit your business. These experts possess in-depth knowledge and expertise in handling complex financial responsibilities such as job costing, payroll taxes, and reporting.

The primary objectives are to safeguard project budgets, track costs https://www.inkl.com/news/the-significance-of-construction-bookkeeping-for-streamlining-projects and revenue, reduce expenses, and ensure efficient project management. Construction accounting is a highly specialized type of financial management because of the industry’s unique characteristics. Unlike many other types of businesses, construction companies need to track and account for multiple contracts, construction projects, and job costs at any given time. This makes keeping tabs on all the moving pieces much more complex than in other industries. For construction businesses, managing accounts payable requires a unique blend of job-specific tracking, vendor management, and cost control. By selecting the right AP software, you can streamline these processes, reduce administrative time, and improve project profitability.

Fluctuating Overhead Costs

Often called pay application or pay apps, the payment application report is a series of documents that contractors exchange with one another during payment. Accounting for construction in progress often seems elusive to many construction contractors. In simple terms, the earned value report allows contractors to respond to project-wise issues more quickly as they can identify them sooner. As is often the case in construction, workers have to switch between job sites in multiple states and cities. In turn, this allows employees to have multiple tax withholdings on a single payroll. Construction is one of those rare industries that face rigorous compliance requirements, followed by multiple profit centers and decentralized production.

Beyond the office walls, Zach’s weekends are filled with adventure, whether he’s exploring Florida’s hidden gems with his wife or battling it out in tournaments. When it’s time to unwind, you’ll find him at the movies or casting his line out for a relaxing fishing session. At work, Justice is passionate about helping the team make decisions and connections that propel the business forward. He prioritizes client satisfaction by serving as a medium to facilitate communication to the proper channels making sure every issue is properly addressed. Features, such as timecards, can be synced automatically while working remotely so that nothing slips through the cracks. If you want to unlock advanced estimating and bill management, you will want the Advanced plan for $699 per month.

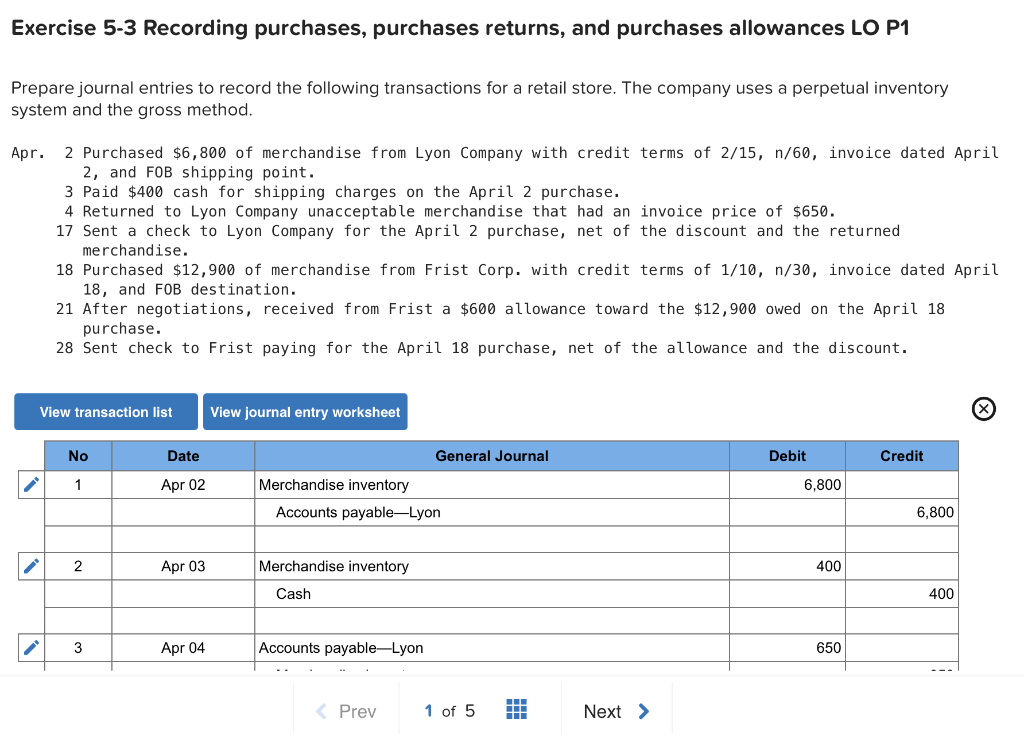

This method contrasts with the gross price method, where purchases are initially recorded at their gross price and a purchase discount is only recorded if payment is made within the discount period. We learned that shipping terms tell you who is responsible for paying for shipping. Free on board (FOB) destination means the seller is responsible what are building automation systems bas for paying shipping and the buyer would not need to pay or record anything for shipping. Free on board (FOB) shipping point means the buyer is responsible for shipping and must pay and record for shipping. In the accounting department, you have matched up the receiving documents sent with this invoice and it is now ready to be paid.

What is the approximate value of your cash savings and other investments?

The discount cannot be taken during the “yellow shaded” days (of which there are twenty). What is important to note here is that skipping past the discount period will only achieve a twenty-day deferral of the payment. There are approximately 18 twenty-day periods in a year (365/20), and, at 2% per twenty-day period, this equates to over a 36% annual interest rate equivalent.

Accounting For Purchase Discounts: Net Method Vs Gross Method

FOB specifies which party (buyer or seller) pays for which shipment and loading costs and where responsibility for the goods is transferred. The last distinction is important for determining liability for goods lost or damaged in transit from the seller to the buyer. International shipments typically use “FOB” as defined by the Incoterm standards, where it always stands for “Free On Board”. Or Canada often use a different meaning, specific to North America, which is inconsistent with the Incoterm standards.

This approach can significantly impact how companies report their finances, offering potential benefits in terms of accuracy and clarity.

Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications.

The Purchases account is usually grouped with the income statement expense accounts in the chart of accounts.

Conversely, the perpetual inventory system involves more constant data update and is a far superior business management tool.

By recording the net amount, companies can more accurately reflect their actual financial obligations and revenues, leading to a clearer financial picture.

Construction Accounting 101: Expert Guide for Contractors

The net method in financial accounting offers a streamlined approach to recording transactions, particularly when dealing with discounts and payment terms. It provides a more accurate representation of cash flow and financial health by recognizing potential savings upfront, leading to improved decision-making for businesses focusing on cost management and efficiency. Another important consideration when using the net method is the treatment of uncollectible accounts. Since the net method records transactions at their net amounts, any subsequent realization that a receivable is uncollectible requires adjustments to the financial statements.

When employing the net method, calculating discounts becomes an integral part of the initial transaction recording. This approach requires businesses to anticipate the discount at the time of purchase or sale, rather than waiting until the payment is made. For example, if a company purchases goods worth $10,000 with a 2% discount for early payment, the transaction is recorded at $9,800. This proactive recording ensures that the financial statements reflect the most accurate and realistic figures. Perpetual inventory system is a technique of maintaining inventory records that provides a running balance of cost of goods available for sale and cost of goods sold for a period. Under this system, no purchases account is maintained because inventory account is directly debited with each purchase of merchandise.

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Accounts payable are recorded at their expected cash payment at the time of purchase. If the payment is made within the discount period, Accounts Payable should be debited, and Cash should be credited for the amount at which the payable was originally recorded. For example, if there was a 2% discount on the above purchase, it would amount to $200 ($10,000 X 2%), NOT $208 ($10,400 X 2%).

In this section, we illustrate the journal entry for the purchase discounts for both net methods vs gross method under the periodic inventory system. Accounting for purchase discounts, we can be recorded under either the net method or the gross method. Both methods provide the same result; however, the accounting journal entry is slightly different. In both cases, the accounts receivable subsidiary ledger is updated, but not inventory, because we don’t do that under the periodic method. The Bryan accounts receivable subsidiary ledger now shows that Geyer owes $16,700, and a call or letter to Geyer would verify that their accounts payable matches if they are using the gross method.

Understanding its concepts, calculations, and applications is essential for businesses aiming to optimize their financial reporting practices. If the invoice is paid within the first ten days, Big Guitar, LLC would be able to record the payoff at the discounted price. Furthermore, the use of the account, Purchase Discounts Lost; highlights the total cost of not paying within the discount period. Importantly, storage costs, insurance, interest and other similar costs are considered to be period costs that are not attached to the product. Instead, those ongoing costs are simply expensed in the period incurred as operating expenses of the business. Take a moment and look at the invoice presented earlier in this chapter for Barber Shop Supply.

The net price method, also known as the net method, is an accounting technique used to record purchases and discounts. Under this method, purchases are recorded at their net price, which is equal to the gross price (the original price) minus any purchase discounts available. Before we dive into the COGS details for the periodic system, begin to familiarize yourself with this chart. This is a quick way to compare the differences between how the two methods record the details involved with inventory. Notice that we did not post the purchases to the inventory account, which is a major difference between this periodic system and the perpetual system.

This is usually expressed as a percentage and is typically provided for in the terms of sale. Some may post the charge as an offset to the expense, as an offset to a payable, or as an income item. The F.O.B. point is normally understood to represent the place where ownership of goods transfers. From 1 January 2024 the following principles relating to the carryover of annual leave apply.

By recording this adjustment, the accounts payable need to be adjusted back to the full invoice amount. Acas provide free and impartial advice to employers and workers on employment matters. The net method works by recording any purchase discounts obtained from suppliers as an immediate offset to the cost of goods purchased. Net method of recording purchase discounts is a method of recording purchase discounts in which the purchase and accounts payable are recorded at the net of the allowable discount. The gross method may inflate sales and purchase figures initially, potentially skewing metrics such as profit margins and return on sales. This can provide a different perspective on operational efficiency and profitability compared to the net method, where discounts are embedded in the initial transaction entries.

The financial statements of most companies are audited annually by an external CPA firm. Auditors play a critical role in ensuring compliance with financial regulations by examining financial statements and accounting records to identify any potential violations. Companies must also take steps to undercapitalization: definition causes and examples ensure compliance by establishing effective internal controls and regularly monitoring their financial reporting processes. Failure to comply with financial regulations can result in significant legal and financial consequences, including fines, penalties, and reputational damage. In addition to financial reporting, accounting also plays a vital role in business decision-making. By analyzing financial data, accounting professionals can identify trends and patterns that can help management make informed decisions regarding the company’s operations.

It’s similar to financial accounting, but this time, it’s reserved for internal use, and financial statements are bank draft definition made more frequently to evaluate and interpret financial performance. An accountant is a professional with a bachelor’s degree who provides financial advice, tax planning and bookkeeping services. They perform various business functions such as the preparation of financial reports, payroll and cash management. Financial accounting is a specific branch of accounting involving a process of recording, summarizing, and reporting the myriad of transactions resulting from business operations over a period of time.

Principles of Financial Accounting

It ensures that financial reports are transparent and reliable, which is essential for making informed business decisions.

Audits are conducted by independent auditors who are responsible for examining financial statements and accounting records to determine whether they are free from material misstatement.

All of our content is based on objective analysis, and the opinions are our own.

This information is used to make informed decisions about investments, financing, and operations.

Financial analysts use this information to assess the liquidity and solvency of a company.

Though many businesses leave their accounting to the pros, it’s wise to understand the basics of accounting if you’re running a business. To help, we’ll detail everything you need to three types of cash flow activities know about the basics of accounting. At its core, accounting is a money-management process that tracks and records expenses. Accountants analyze the flow of cash through your business to improve operations. A great accountant can improve profitability just by managing your finances. For example, they might recommend an online payroll service to cut overhead costs.

Bill and invoice tracking

Financial accounting plays a critical part in keeping companies responsible for their performance and transparent regarding their operations. The accrual method of financial accounting records transactions independently of cash usage. Revenue is recorded when it is earned (when a bill is sent), not when it actually arrives (when the bill is paid). Accrual accounting recognizes the impact of a transaction over a period of time. U.S. public companies are required to perform financial accounting in accordance with generally accepted accounting principles (GAAP).

By prioritizing transparency and accuracy in their financial reporting, companies can demonstrate their commitment to responsible business practices and build a strong foundation for long-term success. It provides the necessary information to evaluate the financial performance, health, and stability of an organization. Financial analysis involves the use of accounting data to assess the financial position of a company and make informed decisions. Internal auditing is when the company’s finances are audited by accountants who work for that company. It’s typically done by tax, financial or managerial accountants, depending on the audit’s purpose. Cost accountants track the company’s spending across these three areas and create internal reports that break it down.

International Financial Reporting Standards (IFRS)

They must also have effective internal controls in place to prevent errors and fraud. It ensures that financial reports are transparent and reliable, which is essential for making informed business decisions. Accounting is popularly regarded as “the language of business” because it doesn’t just help you keep track of your money, but also helps you make informed decisions about your business. To speed up action, you may hire accounting professionals or purchase accounting software to ensure accurate financial audits and reporting. You can choose to manage your business accounting by hiring an in-house accountant or CPA.

Therefore, it is crucial that all financial reports are accurate and up-to-date. Another important function of accounting in financial analysis is to provide information on the cost of goods sold. This information is crucial in determining the profitability of a company. Financial analysts use this information to calculate gross profit margin and net profit margin. Accounting is an essential tool for businesses to make informed decisions.

Types of Accounting

On the flip side, accountants use invoicing software to help you get paid. Instead of tying expenses to a product or service you offered, tie them into their return on investment. In recent years, there has been a growing demand on the part of stakeholders for information concerning the social impacts of corporate decision making. Increasingly, companies are including additional information about environmental impacts and risks, employees, community involvement, philanthropic activities, and consumer safety. Much of the reporting of such information is voluntary, especially in the United States. Members of financial accounting can carry several different professional designations.